7 Proven Wealth Management Services for HNWIs in India

Wealth Management Services are often the missing link for investors who realize that a “Buy” button is not a substitute for a strategy. In the early stages of wealth creation, a DIY approach feels empowering. You download a sleek app, set up a few Systematic Investment Plans (SIPs), and watch the charts move upward. It’s convenient, low-cost, and effective for the “accumulation phase.”

However, there is a silent threshold—usually when a portfolio crosses the ₹50 Lakh to ₹1 Crore mark—where the complexity of your assets begins to outpace the capabilities of a smartphone interface. For HNWIs India presents a unique challenge: the goal is no longer just “investing,” but the sophisticated orchestration of tax efficiency, risk mitigation, and estate planning. This is where the limitations of DIY apps become a liability. When your financial life involves multiple income streams, evolving tax brackets, and long-term legacy goals, you don’t need a better algorithm; you need comprehensive Wealth Management Services.

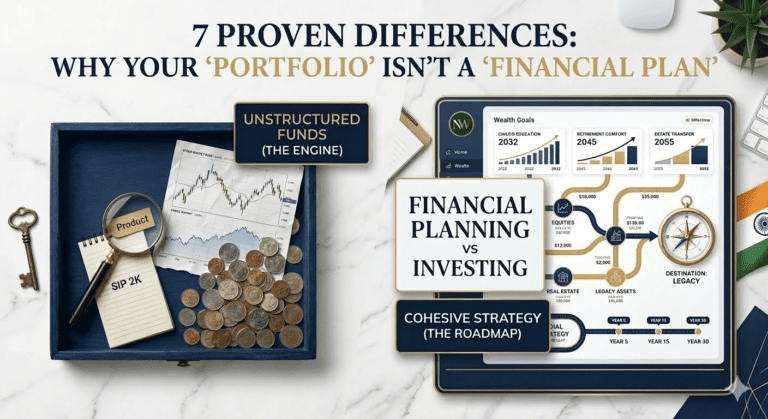

The “App Trap”: Why Execution is Not Strategy

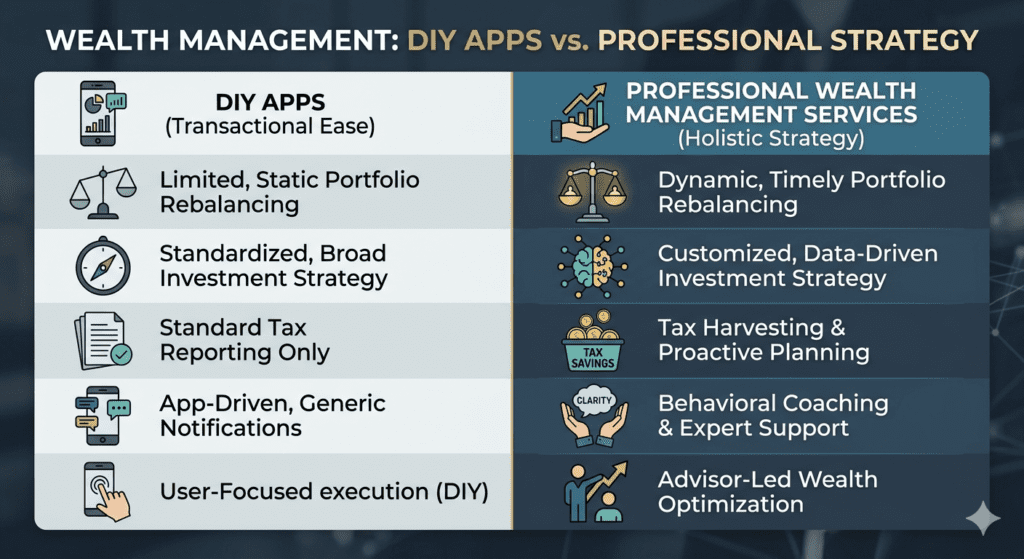

The primary misconception among modern investors is confusing transactional ease with strategic wisdom. Apps are built for execution—they are digital order-takers. They can help you buy a fund, but they cannot tell you if that fund still fits your risk profile after a 20% market correction or a change in the Finance Regulation.

1. The Hidden Cost of DIY Errors

As your capital grows, the cost of a 1% error in your investment strategy isn’t just a few thousand rupees; it’s lakhs of rupees in missed opportunities or unnecessary tax leakages. Professional wealth management shifts the focus from “Which fund is performing today?” to “How does this asset protect my purchasing power over the next decade?”

2. Beyond the Buy Button

DIY apps rarely prompt you to exit a position. They are designed to keep you “invested.” A professional advisor, however, provides the emotional arbitrage needed to prune underperforming assets and lock in gains, ensuring your portfolio remains lean and goal-aligned.

Critical Pillars of High-Tier Wealth Management Services

To transition from a “retail investor” to a “wealthy family,” several sophisticated layers must be added to your financial architecture.

Portfolio Rebalancing: The Art of Risk Control

Market movements naturally drift your portfolio away from its original intent. If equities surge, your 60/40 split might become 80/20, exposing you to catastrophic risk just before a downturn. Portfolio rebalancing is the disciplined process of selling high and buying low—a task most DIYers ignore because it feels counterintuitive to sell “winners.”

Tax Harvesting and Efficiency

In India, the tax landscape is a moving target. From LTCG changes to the taxation of debt-oriented mutual funds, a professional wealth manager implements tax-loss harvesting. This involves strategically realizing losses to offset capital gains, potentially saving you significant outflows every financial year.

Why HNWIs in India are Moving Away from DIY

The Indian market is uniquely volatile and highly regulated. For HNWIs India represents a land of opportunity, but only for those who can navigate the nuances of the SEBI and RBI mandates.

3. Access to Exclusive Opportunities

High-ticket wealth management provides access to Alternative Investment Funds (AIFs), Pre-IPO opportunities, and Structured Products that are simply not available on retail DIY apps. These instruments allow for “uncorrelated returns,” meaning your wealth isn’t solely dependent on the Nifty 50’s performance.

4. Holistic Financial Planning

A financial planner does not look at your stocks in a vacuum. They look at your business liabilities, your children’s international education costs, and your retirement lifestyle. They integrate insurance, debt management, and cash flow analysis into a single, cohesive roadmap.

📢 Join the Finanshull Community!

Want to stay ahead of the curve with daily insights on market trends, wealth psychology, and financial discipline? Join thousands of smart investors on our Finanshull Instagram and YouTube channels. Get the clarity you need to move from “saving” to “building a legacy.” [Follow us on Instagram] | [Subscribe on YouTube]

The Human Element: When Math Meets Emotion

Algorithms are excellent at math, but they are terrible at psychology. When the market enters a bear phase, an app sends a generic notification. A wealth manager picks up the phone.

5. Behavioral Coaching

The greatest threat to wealth isn’t market volatility; it’s investor behavior. During a market crash, the “human filter” prevents panic selling. During a bull run, it prevents “FOMO” (Fear Of Missing Out) into overvalued sectors. This behavioral coaching is perhaps the most undervalued component of wealth management services.

6. Complex Goal Sequencing

Life doesn’t happen in a linear fashion. You might decide to start a new venture or move abroad. A DIY app cannot recalibrate your entire life’s savings for a “what-if” scenario. A human strategist uses sophisticated Monte Carlo simulations and stress-testing to ensure your plan survives real-world chaos.

Strategic Asset Allocation vs. Asset Collection

Most DIY investors are “asset collectors.” They have 15 different mutual funds, 4 insurance policies, and some random stocks. This creates “diworsification”—redundancy that adds risk without increasing return.

A dedicated financial planner focuses on Strategic Asset Allocation. According to various studies, over 90% of a portfolio’s return variability is determined by asset allocation, not individual stock picking. We ensure your assets are distributed across geographies and classes (Gold, Real Estate, Equity, Fixed Income) to provide a smoother ride.

Final Thoughts: The Transition to Mastery

There is a point in every successful professional’s life where their time becomes more valuable than the “cost” of professional advice. If you are spending your weekends managing spreadsheets and tracking NAVs, you are working for your money. Wealth Management Services ensure that your money is working for you.

At Nemi Wealth, we don’t just manage portfolios; we manage futures. We provide the “Advice Filter” that separates market noise from actionable intelligence. It’s time to move beyond the app and enter the world of bespoke financial engineering.

External Resources for Further Reading:

Ready to Elevate Your Wealth Strategy?

Your wealth deserves more than a “swipe-to-invest” interface. It requires a partner who understands the intricacies of the Indian economy and the nuances of your personal goals.

[Book a Private Consultation with Nemi Wealth Today] Let’s build a personalized roadmap that turns your success into a lasting legacy.