Securing Your Future: 3 Powerful Ways Insurance Protects Your Wealth and Future in India

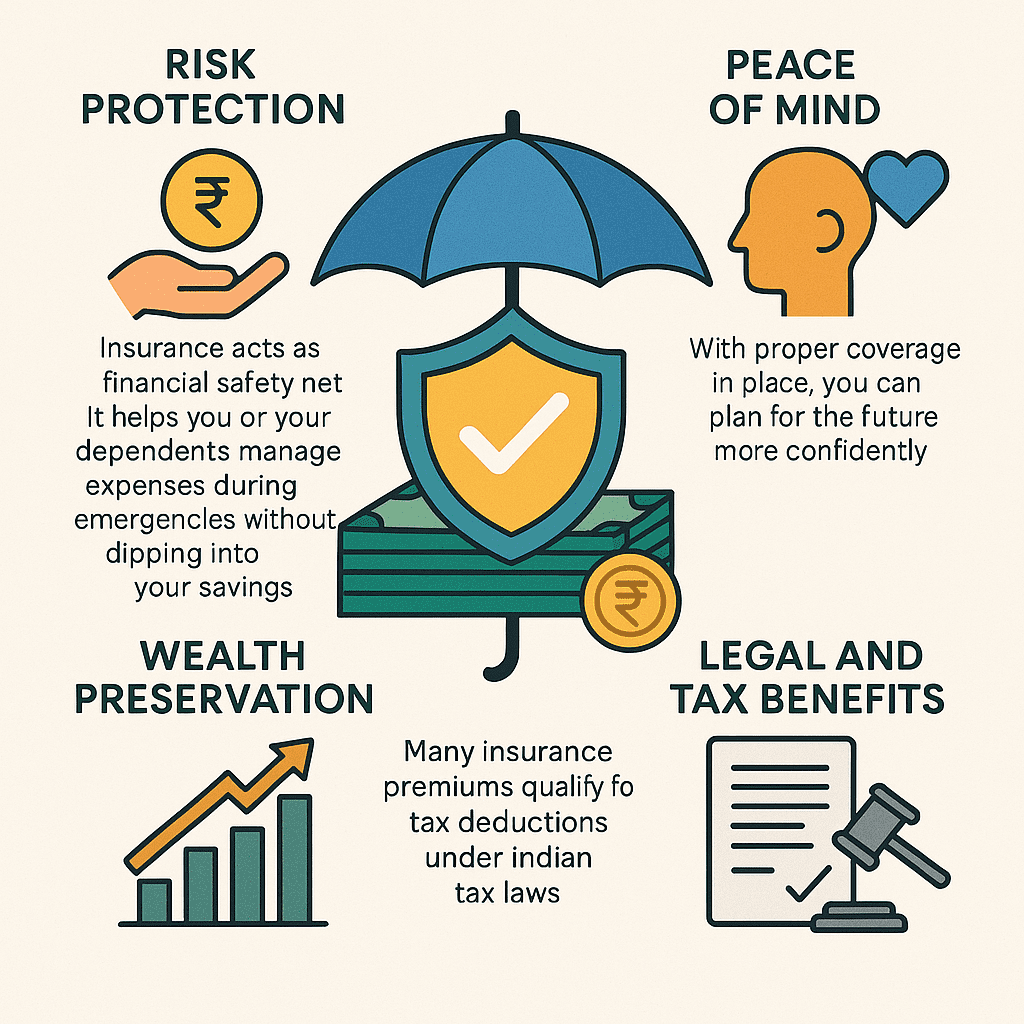

Financial planning is not just about saving or investing for the future it’s about building a resilient system that can withstand unexpected financial shocks. One of the most overlooked, yet crucial, components of a sound financial plan is risk management. And in personal finance, managing risk often begins with the right kind of protection insurance.

In India, with rising healthcare costs, increasing life expectancy, and greater economic volatility, insurance is no longer optional. It is a necessity for anyone aiming for financial security. This article explores the significance of insurance in financial planning and delves into three essential insurance products in India: health insurance, term plans, and endowment policies.

Why Is Insurance Vital to Financial Planning?

The foundation of a strong financial plan is the ability to manage unforeseen risks. Whether it’s an accident, illness, or an untimely death, such events can derail years of careful savings and investments if you’re unprotected.

Here’s why insurance should be part of your financial strategy:

Health Insurance: Protection Against Medical Expenses

Medical inflation in India has been rising at double-digit rates. Even a short hospital stay can cost lakhs of rupees. Without adequate health coverage, these expenses can drain your savings or push your family into debt.

What Is Health Insurance?

Health insurance is a contract in which the insurance provider agrees to cover medical expenses incurred due to illnesses, accidents, or surgeries. In return, you pay a premium, usually annually.

Key Benefits of Health Insurance

- Cashless Hospitalization: Empanelled hospitals offer cashless services, meaning you don’t have to pay upfront.

- Pre and Post-Hospitalization Coverage: Many plans cover expenses like diagnostic tests, medicines, and doctor visits.

- Daycare Procedures: Surgeries that don’t require 24-hour hospitalization (like cataract or chemotherapy) are also covered.

- Tax Benefits: Under Section 80D of the Income Tax Act, premiums paid towards health plans qualify for tax deductions up to ₹25,000 for self and family, and an additional ₹25,000 for parents (₹50,000 if they are senior citizens).

Types of Health Insurance in India

- Individual Health Insurance: Covers hospitalization and treatment for a single policyholder.

- Family Floater Plan: Covers the entire family (usually self, spouse, and children) under one sum insured.

- Senior Citizen Health Plan: Tailored for individuals aged 60 and above with higher coverage and relevant features.

- Critical Illness Insurance: Offers a lump sum on diagnosis of critical illnesses like cancer, kidney failure, or cardiac arrest.

Choosing the Right Health Plan

- Look for plans with lifetime renewability.

- Check the network of hospitals for cashless treatment.

- Understand waiting periods for pre-existing diseases.

- Read the fine print know what’s excluded from the coverage.

Term Insurance: Ensuring Family Security

Term insurance is a fundamental part of life protection. It provides a large cover at a low premium and is designed solely to protect your family in case of your untimely demise.

What Is Term Insurance?

It is a type of life coverage where the insurer pays a predetermined sum (the “sum assured”) to your nominee if you pass away during the policy period. If you survive the term, there is no maturity benefit (in a pure term plan).

Key Features of Term Insurance

- Affordable Premiums: Especially for younger policyholders.

- High Sum Assured: You can buy coverage of ₹50 lakhs to ₹1 crore or more, depending on income and need.

- Flexible Payout Options: Your nominee can receive the death benefit as a lump sum, regular income, or a mix of both.

- Add-on Riders: Options like accidental death benefit, critical illness, or waiver of premium enhance coverage.

- Tax Benefits: Under Section 80C (premiums) and Section 10(10D) (death benefit), term plans offer tax relief.

Why Every Breadwinner Needs Term Cover

Imagine your family’s monthly expenses, children’s education, or home loan EMIs being handled without your income. Term insurance ensures that your family continues to live with dignity and meets financial goals even in your absence.

Choosing the Right Term Plan

- Choose a sum assured that is at least 10–15 times your annual income.

- Select a policy term that covers your working years.

- Compare policies from multiple providers for claim settlement ratio and premium affordability.

- Avoid unnecessary riders if they don’t fit your actual needs.

Endowment Plans: Protection with Savings

For those looking to combine life cover with a disciplined savings strategy, endowment policies offer the best of both worlds.

What Is an Endowment Plan?

An endowment plan provides both life coverage and a savings corpus at the end of the policy term. Part of your premium goes toward securing your life, and the rest is invested to build a maturity amount.

Key Benefits of Endowment Plans

- Guaranteed Returns: You receive a lump sum if you survive the policy term.

- Life Cover: If the policyholder dies during the term, the nominee receives the death benefit.

- Tax Efficiency: Both premiums (under Section 80C) and maturity proceeds (under Section 10(10D), if conditions are met) are tax-free.

- Riders Available: Additional benefits for critical illness, disability, or accidental death can be attached.

Ideal Use Cases for Endowment Plans

- Saving for a child’s education or marriage

- Building a retirement corpus

- Long-term savings for home purchase or travel

Limitations to Consider

- Lower returns compared to mutual funds or stocks

- Lock-in periods (often 10–15 years)

- Less flexibility than market-linked insurance products

Insurance as a Tool for Financial Discipline

Many people struggle with consistent saving habits. Insurance, particularly endowment and traditional savings plans, enforces financial discipline. You commit to paying premiums regularly, which fosters a savings mindsetAdditionally, these policies inculcate long-term thinking. Unlike stocks or mutual funds, which tempt investors to exit during market volatility, insurance products are generally held for their entire term.

How to Choose the Right Protection Plan

Every individual’s needs are unique, but the following factors can guide your choice:

- Life Stage: A young professional may need a basic term cover, while someone with dependents requires health and life coverage.

- Financial Goals: Are you saving for retirement, children’s education, or a home purchase?

- Risk Tolerance: If you’re risk-averse, endowment plans might appeal to you more than ULIPs or equities.

- Affordability: Don’t over-commit. Choose a plan that fits into your monthly budget.

- Claim Settlement Ratio: Check insurer track records.

- Policy Flexibility: Can you increase coverage or add riders later?

Common Mistakes to Avoid

- Delaying insurance purchase: Premiums are lower when you’re younger and healthier.

- Over-relying on employer health plans: Group coverage may not be sufficient or portable.

- Underinsuring yourself: Ensure your sum assured reflects real expenses.

- Not reviewing policies regularly: Life situations change so should your coverage.

How Nemi Wealth Can Help

At Nemi Wealth, we take a holistic view of your financial needs and recommend the right protection mix tailored to your income, lifestyle, and goals. We help you:

- Assess the right type and amount of coverage

- Compare providers for cost and claim performance

- Build a layered protection strategy with health, life, and savings-based coverage

- Monitor and revise your insurance portfolio annually

By taking expert guidance, you ensure that you don’t just buy a policy but buy peace of mind.

Final Thoughts: Secure Today, Smile Tomorrow

Insurance isn’t just a product— a promise. A promise to your family that they’ll be protected. A promise to yourself that your plans won’t be shattered by misfortune. It’s a quiet force in your financial plan, one that works when you can’t. Health coverage shields you from rising medical costs. Term plans ensure your loved ones aren’t left financially vulnerable. Endowment plans build future wealth while offering life protection. If you haven’t reviewed your insurance portfolio lately, now is the time. Financial planning without protection is like building a house without a roof. Let Nemi Wealth help you make smarter, safer choices because when life is unpredictable, protection is powerful.