Insurance in Financial Planning: 3 Bold Ways to Secure Wealth

You’ve worked hard to build your career, save for your dream home, and invest in the market. But have you ever stopped to wonder how quickly those dreams could evaporate if life threw a curveball? Between the hustle of city life and the mounting pressure of professional responsibilities, most Indians treat insurance as a tax-saving chore rather than a wealth-protection shield.

The reality is that insurance in financial planning is the bedrock upon which all your other investments sit. Without it, you aren’t just investing; you are gambling with your family’s stability. Whether it is a sudden medical emergency or an untimely loss, the right protection ensures that your financial roadmap remains intact even when life gets messy. At Nemi Wealth, we believe in building a resilient system that stands the test of time.

Key Takeaways

- Risk Mitigation: Insurance in financial planning acts as a risk-transfer tool rather than a traditional investment.

- The Trinity of Protection: A robust plan must include Health, Term, and Savings-linked (Endowment) coverage.

- Wealth Preservation: Proper coverage prevents “forced selling” of assets like gold or property during emergencies.

- Tax Efficiency: Leverage Sections 80C and 80D to optimize your outgoings while staying protected.

Understanding the Core: Why Insurance is the Foundation of Wealth

Think of your financial plan as a high-performance car. Your investments are the engine, but insurance in financial planning represents the brakes and the airbags. You hope you never have to use them, but you wouldn’t dare drive at high speeds without them.

In the Indian context, where medical inflation is skyrocketing at nearly 14% annually, a single hospital stay can wipe out three years of SIP contributions. By integrating insurance into your strategy, you aren’t just “buying a policy”—you are securing your peace of mind.

Join the Conversation! Want to see how real Indian families are structuring their portfolios? Follow us on Instagram @finanshull for bite-sized logic, myth-busting reels, and the latest updates on navigating the Indian markets with confidence.

1. Health Insurance: The First Step of Insurance in Financial Planning

Medical expenses are the biggest threat to wealth in India. With medical inflation hitting double digits, the role of health insurance in financial planning has moved from ‘optional’ to ‘mandatory’ for Indian middle-class families. With specialized treatments costing upwards of ₹10 lakhs, relying on your company-provided “Group Insurance” is a risky strategy.

- Cashless Comfort: Access to network hospitals means no frantic calls for cash at midnight.

- Comprehensive Coverage: Look for plans covering pre and post-hospitalization to ensure the “hidden costs” are handled.

- The 80D Edge: Save up to ₹25,000 (and more for parents) in taxes while securing world-class healthcare.

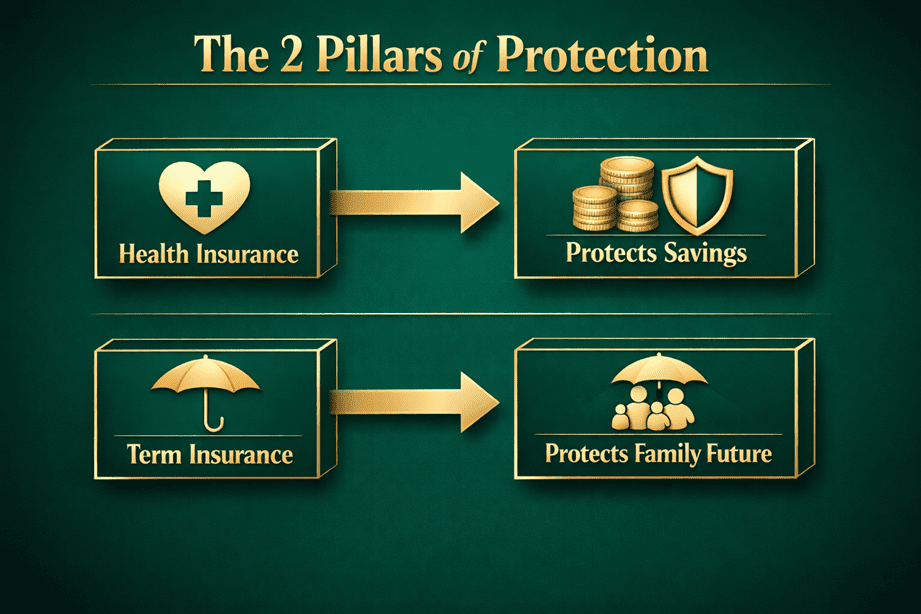

2. Term Insurance: The Purest Form of Insurance in Financial Planning

Term insurance is the purest form of insurance in financial planning. It is low-cost and high-impact. If you are the primary breadwinner, this isn’t optional. It ensures that your children’s education, your spouse’s lifestyle, and your home loans are taken care of, even if you aren’t there to provide.

- Income Replacement: Aim for a sum assured that is 15-20x your annual income.

- Rider Power: Add “Critical Illness” or “Accidental Disability” riders to make your term plan a 360-degree safety net.

[Image Generation Prompt 2: Subject: A high-quality 3D infographic flowchart titled ‘The 2 Pillars of Protection’. Design: Clean vector lines, Deep Emerald background with Champagne Gold text. Flowchart Steps: 1. Health Insurance (Icon: Cross/Heart) -> ‘Protects Savings’. 2. Term Insurance (Icon: Umbrella) -> ‘Protects Family Future’. Alt Text: Infographic showing the role of health and term insurance in financial planning.]

Actionable Steps to Build Your Strategy

Step 1: Protect the Downside (Term & Health)

The first rule of insurance in financial planning is to cover ‘catastrophic risks’—events that could bankrupt a family—before looking at wealth accumulation. Before you buy your first stock, ensure your “Big Two” are in place. Purchase a personal health cover (independent of your employer) and a term plan that covers all your liabilities.

Step 2: Build the Core (Holistic Planning)

A common mistake in insurance in financial planning is treating it as an expense to be minimized rather than an asset to be optimized for maximum protection. Integrate your insurance premiums into your monthly budget. At Nemi Wealth, we help you align these premiums so they don’t feel like a burden but an investment in your safety.

Step 3: Diversify for Alpha (US Equity/SIFs)

Once your protection is set, you can aggressively pursue growth through US Equities, Specialized Investment Funds (SIFs), or domestic Mutual Funds. You can afford to take higher risks here because your foundation is secure.

Frequently Asked Questions

1. Is my company health insurance enough? Usually, no. Company covers are often basic and cease the moment you resign or retire. A personal plan ensures continuity and higher coverage limits.

2. At what age should I buy a term plan? As early as possible. Premiums for insurance in financial planning are significantly lower when you are in your 20s or 30s and stay locked in for life.

3. Do endowment plans offer good returns? They offer “safe” returns. While they may not beat a mid-cap fund, they provide the guarantee and discipline that equity cannot offer, making them perfect for “must-meet” goals.

4. What is a Claim Settlement Ratio (CSR)? It is the percentage of claims an insurer pays out. Always look for insurers with a CSR consistently above 97% to ensure reliability.

5. Can I have multiple insurance policies? Yes. You can have multiple term plans, but you must disclose all previous policies to the insurer to avoid claim rejection.

6. Why is insurance in financial planning considered a foundation? Because it protects your existing assets from being liquidated during an emergency.

Financial planning without protection is like building a skyscraper on sand. It might look impressive, but it won’t survive the first storm. By prioritizing insurance in financial planning, you are making a rational, empathetic choice for your family’s future. You aren’t just saving money; you are buying the right to remain wealthy, no matter what happens. Ultimately, mastering insurance in financial planning ensures that your wealth-building journey isn’t derailed by life’s uncertainties.

Secure your legacy today. Consult with the experts at Nemi Wealth to evaluate your current coverage and build a bulletproof financial shield. Let’s make your money work as hard as you do.