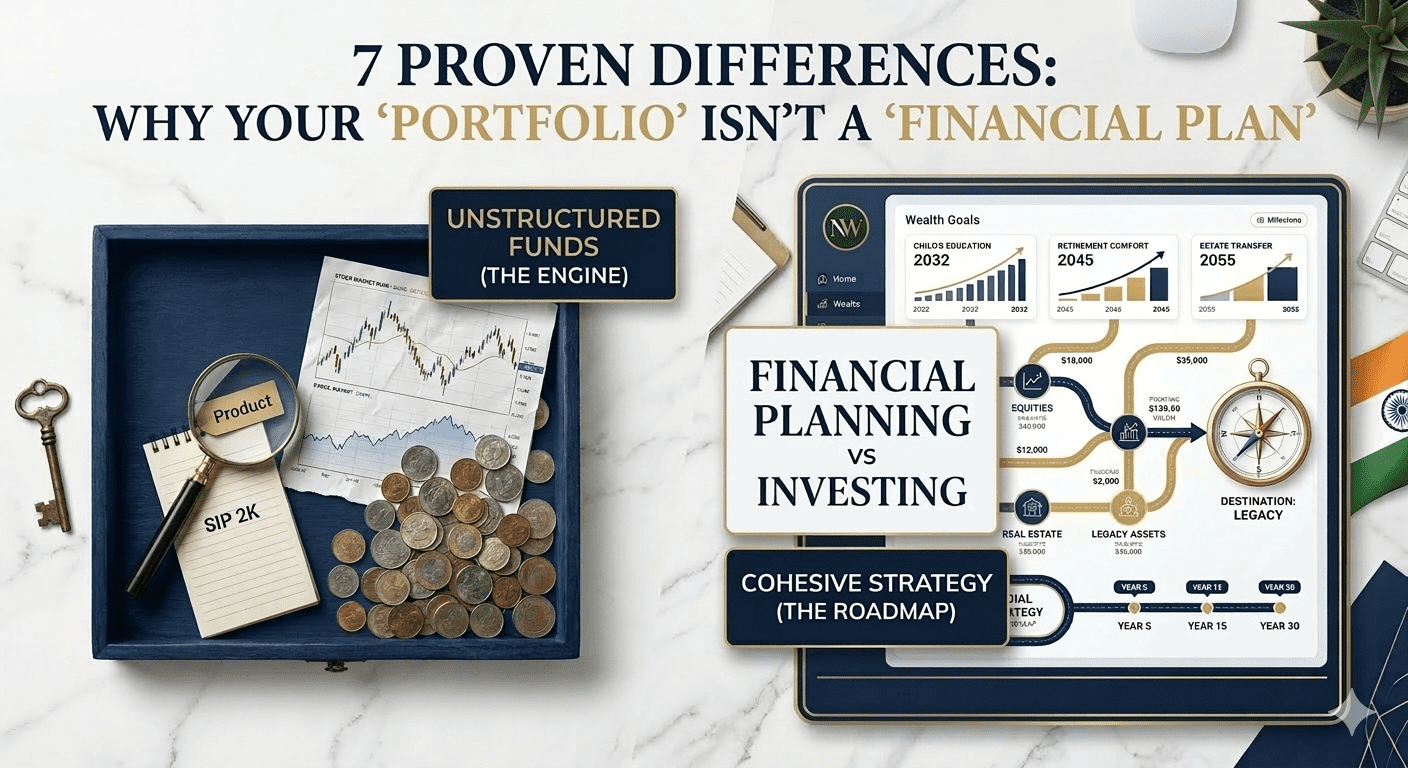

7 Proven Differences: Why Your ‘Portfolio’ Isn’t a ‘Financial Plan’

In the world of high-net-worth wealth management, there is a common misconception that often leads to stagnant growth or unexpected tax burdens: the belief that owning a diverse collection of mutual funds or stocks constitutes a financial strategy.

For many busy professionals, “investing” is something done in fragments—an SIP here, a tax-saving bond there, and perhaps a PMS suggested by a bank RM. However, without a cohesive structure, you don’t have a strategy; you have a junk drawer of financial products. Understanding the nuances of financial planning vs investing is the first step toward moving from “buying products” to “building a legacy.”

At Nemi Wealth, we see this daily. Clients come to us with impressive portfolios that are unfortunately decoupled from their actual life milestones. This post explores why your portfolio is merely the engine, while your financial plan is the GPS, the driver, and the destination.

1. The Core Philosophy: Strategy vs. Tactics

Investing is a tactical exercise. It is the act of allocating capital to specific assets—equities, debt, or gold—to generate a return.

Financial planning, conversely, is the overarching strategy. It is the holistic process of looking at your current net worth, your cash flow, your liabilities, and your aspirations. While investing asks, “Which fund will give me 15%?”, financial planning asks, “How much risk can I afford to take to ensure my child’s Ivy League education is funded regardless of market volatility?”

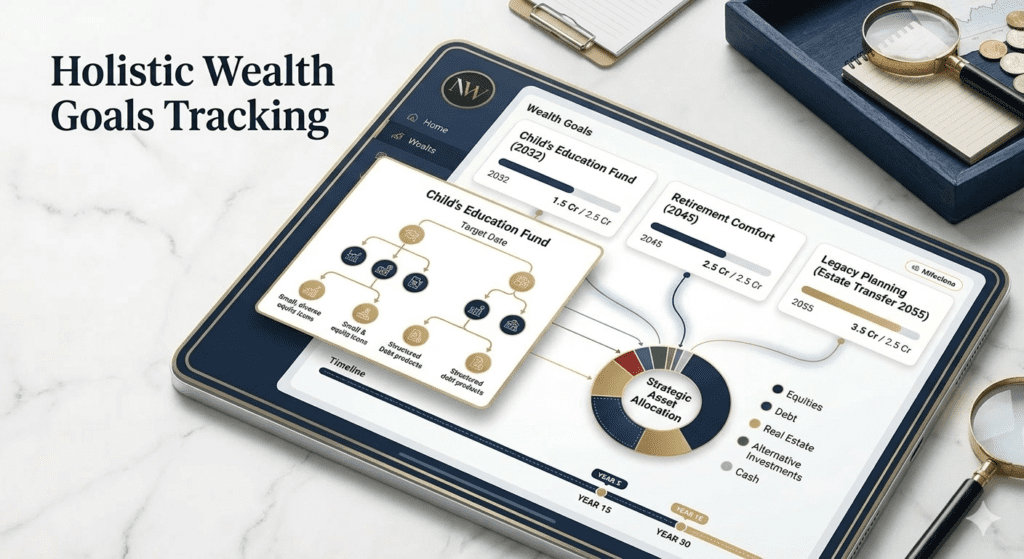

2. Wealth Goals: The “Why” Behind the “What”

A portfolio is often built on the “What”—what is performing well right now? This leads to “chasing returns,” a dangerous game for HNWIs.

Effective wealth goals are the foundation of a true financial plan. These goals are quantified, time-bound, and prioritized:

- Lifestyle Maintenance: Ensuring your post-retirement lifestyle doesn’t dip.

- Estate Planning: Transitioning wealth to the next generation with minimal friction.

- Philanthropy: Creating a structured impact.

Without these goals, portfolio management becomes a rudderless ship. You might be “beating the index,” but if your liquidity is tied up when you need to purchase a primary residence or fund a business expansion, the “returns” are irrelevant.

3. The Role of Portfolio Management in the Big Picture

Don’t mistake the part for the whole. Portfolio management is a subset of your financial plan. It is the technical execution of the asset allocation dictated by the plan.

A professional wealth strategy involves:

- Asset Location: Deciding which assets should be in which family member’s name for tax efficiency.

- Rebalancing: Ensuring a bull run in mid-caps hasn’t skewed your risk profile beyond your comfort zone.

- Risk Mitigation: Integrating insurance and emergency liquidity so the portfolio never has to be liquidated at a loss.

Stay Informed with the Experts: Managing wealth requires more than just reading the news; it requires a mindset shift. Join our Finanshull community on Instagram and YouTube for daily deep dives into wealth psychology and sophisticated financial insights.

4. Why You Need a Financial Advisor in India

The Indian market is unique. With shifting tax regimes (like the recent changes to LTCG and debt fund taxation) and a volatile emerging market landscape, the “DIY” approach often leads to “leaky” wealth.

A dedicated financial advisor in India provides the “Advice Filter.” They act as a behavioral coach, preventing you from making emotional exits during market corrections or over-leveraging during bull runs. They ensure that your financial planning vs investing ratio is balanced, focusing on net-of-tax, inflation-adjusted returns rather than gross numbers.

5. Risk Management: Protection vs. Growth

Investing focuses on “Market Risk”—the chance that your stocks might go down. Financial planning focuses on “Personal Risk”—the chance that your plan might fail.

A portfolio doesn’t care if you become incapacitated or if a legal suit hits your business. A financial plan, however, incorporates:

- Succession Planning: Ensuring your family is taken care of.

- Liability Management: Balancing business debt with personal assets.

- Tax Planning: Utilizing tools like the Income Tax Department guidelines to optimize your outflows.

6. Time Horizon and Liquidity

Investing often operates in cycles—3 years, 5 years, or “until the market hits a peak.” A financial plan operates on a lifetime horizon.

It dictates your liquidity needs. For instance, if you have a wealth strategy that includes a daughter’s wedding in two years, a professional planner would move those specific funds into low-volatility instruments, regardless of how “hot” the equity market is. An investor without a plan might keep that money in small-caps, risking a 30% drawdown right when the check needs to be written.

7. Performance Measurement: Benchmark vs. Milestones

In the financial planning vs investing debate, the way you measure success changes:

- Investing Success: “I beat the Nifty 50 by 2% this year.”

- Planning Success: “I am 15% closer to my early retirement goal, and my family’s lifestyle is fully hedged against inflation.”

The Verdict: You Need a Roadmap, Not Just an Engine

A portfolio is a collection of products; a financial plan is a roadmap to your life’s purpose. While you can buy a fund online with a click, you cannot “buy” a strategy that accounts for your specific family dynamics, tax bracket, and long-term legacy.

At Nemi Wealth, we specialize in transforming disorganized portfolios into streamlined, goal-oriented wealth engines. We don’t just pick funds; we architect futures.

Explore our Wealth Management Services to see how we align portfolios with plans.

Understand the latest regulatory protections for investors from SEBI.

Ready to elevate your wealth strategy?

Stop collecting products and start building a plan. Your wealth deserves the precision of a professional roadmap.

Book a Private Consultation with Nemi Wealth Today. Let’s align your portfolio with your life goals.