Financial Planning for Indian Women: 5 Essential Steps

Picture this: You are a multi-tasking pro, managing a high-pressure career or a complex household (or both!) with surgical precision. Yet, when the conversation shifts to mutual fund portfolios, tax harvesting, or asset allocation, do you find yourself leaning on your father, brother, or husband to take the wheel? You aren’t alone. For decades, the “money talk” in Indian households has been a male-dominated territory, leaving many women as spectators of their own wealth.

However, the reality of the 21st century is different. Whether you are a corporate leader or a home manager, understanding financial planning for Indian women is no longer a luxury—it is a survival skill. True empowerment isn’t just about earning a paycheck; it’s about having the agency to decide where that money goes. In this guide, we will break down why women need a unique approach to money and how you can transition from a “saver” to a “wealth creator.”

Key Takeaways

- Customization Matters: A generic financial plan rarely accounts for women’s unique career breaks and life stages.

- Independence is Key: Relying on others for financial decisions limits your life choices and long-term security.

- Longevity Risk: Women statistically live longer than men, meaning your retirement corpus needs to last much longer.

- Investment > Saving: Keeping money in a savings account or “gold in the locker” is not enough to beat inflation.

Why “One Size Fits All” Fails in Financial Planning for Indian Women

Most financial products are designed with a linear career path in mind—the traditional 25-to-60-year work cycle. But for many Indian women, life isn’t a straight line. Career breaks for childcare, caregiving for elderly parents, or a later-than-usual entry into the workforce are common realities. This is precisely why financial planning for Indian women must be distinct from the plans designed for men.

We must also address the biological reality: women generally have a longer life expectancy than men. While living longer is a blessing, it requires a larger retirement corpus. If your spouse is the sole “planner” and passes away earlier, you may be left managing a complex portfolio you don’t understand, or worse, find that the funds are insufficient for your sunset years. Proper financial planning for Indian women bridges this gap, ensuring that your money outlives you, not the other way around.

Want quick, daily insights on personal finance? Join our community on Instagram @finanshull for bite-sized tips.

The Elephant in the Room: Direct vs. Regular Plans

As you embark on your journey of financial planning for Indian women, you will encounter the debate between “Direct” and “Regular” mutual fund plans. Direct plans have lower expense ratios because you manage them yourself. However, this is only beneficial if you have the hours to research thousands of funds, track market volatility, and rebalance your portfolio quarterly.

At Nemi Wealth, we believe that for a busy woman, time is the most valuable asset. Regular plans include the cost of a professional who acts as your financial co-pilot. This isn’t just about picking a fund; it’s about emotional hand-holding during market crashes and ensuring your asset allocation remains aligned with your goals. A DIY approach is great if you are an expert, but having a professional ensures that your financial planning for Indian women remains consistent even when life gets hectic.

Top 10 Money Mistakes Women Make

Before we build, we must identify the cracks. Many women fall into these common traps:

- The “Saving” Trap: Thinking that keeping cash in a cupboard or a 3% interest savings account is “investing.”

- Delegating Decisions: Letting a male relative make all the choices without understanding the “why” behind them.

- Underestimating Insurance: Relying solely on a husband’s corporate health cover.

- Emotional Investing: Buying gold as the only investment because it “feels” safe, despite its storage costs and liquidity issues.

- Ignoring the Gap: Not accounting for the impact of career breaks on EPF and gratuity.

- Prioritizing Others: Saving for a child’s wedding before securing one’s own retirement.

- Small-Goal Syndrome: Setting tiny targets because of a lack of confidence in market returns.

- Lack of Nominations: Forgetting to update nominees on bank accounts and investments.

- Fear of Risk: Avoiding equity entirely, which leads to wealth erosion by inflation.

- The “Later” Mentality: Waiting for the “perfect” time to start investing.

Actionable Steps to Build Your Strategy

Effective financial planning for Indian women follows a logical hierarchy. You cannot build a skyscraper on a foundation of sand. Here is how we recommend you structure your wealth:

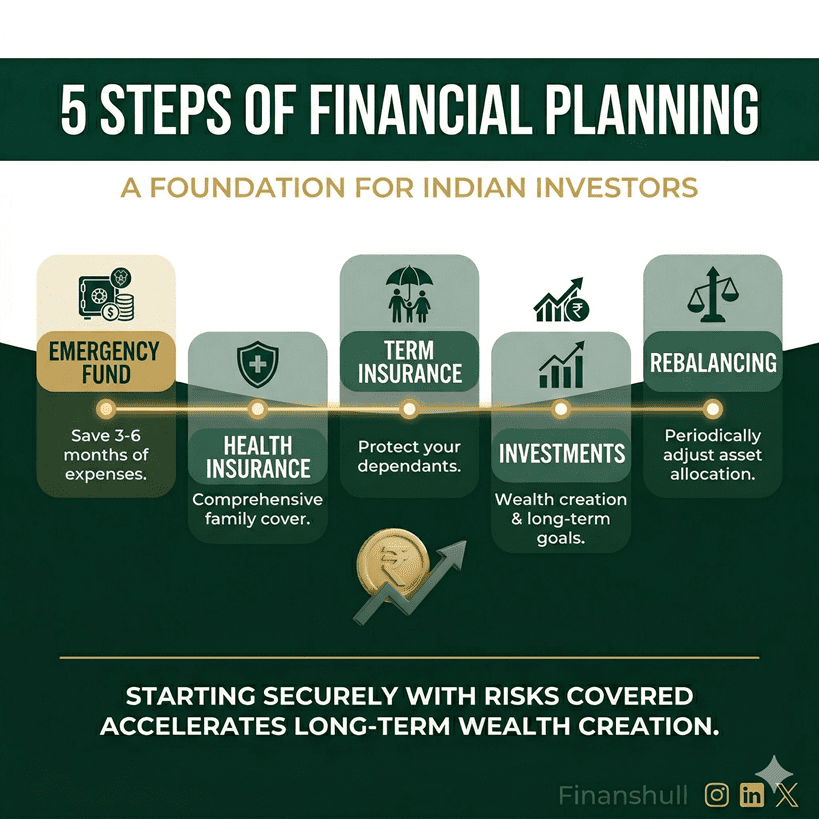

Step 1: Protect the Downside

Before you think about returns, think about risks. Every woman needs her own Health Insurance, independent of her employer or spouse. Critical illness covers are especially important given the rising costs of female-specific health issues. Furthermore, if you have dependents, a Term Insurance policy is non-negotiable. It is the cheapest way to buy peace of mind.

Step 2: Build the Core

The core of your financial planning for Indian women should be an Emergency Fund. This should cover 6–12 months of your expenses in a liquid format. Once this is ready, we move to Mutual Funds. This is where “saving” becomes “growing.” By using a mix of Large-cap, Mid-cap, and Debt funds, you can create a portfolio that reflects your specific risk appetite and life goals, whether that’s a solo trip to Europe or early retirement.

Step 3: Diversify for Alpha

Once the basics are solid, look at international diversification. US Equity or specialized Structured Investment Funds (SIFs) can provide that extra “alpha” or higher returns. Diversifying outside the Indian economy protects your wealth against rupee depreciation, making it a sophisticated move in the journey of financial planning for Indian women.

Conclusion

Taking charge of your finances is the ultimate act of self-care. It transforms “what if” into “what’s next.” Remember, financial planning for Indian women is not about restricted spending; it is about creating a life of choices. You don’t need to be a math genius to start; you just need the discipline to begin and the right partner to guide you through the complexities of the market.

Managing all of this alone can be overwhelming. If you want a tailored roadmap for your wealth, let’s build a personalized financial plan together. Get Started Here.

Is gold a good investment for Indian women?

Gold is a great cultural asset and a hedge against inflation, but it shouldn’t be your only investment. In financial planning for Indian women, we recommend limiting gold to 5-10% of your portfolio, preferably through Gold ETFs rather than physical jewelry. Click here to start investing in Gold ETFs.

I am a homemaker; can I still have a financial plan?

Absolutely. Financial planning is about managing resources, not just a salary. You can start with Small Case investments or SIPs from your household savings. According to SEBI guidelines, anyone with a PAN card can invest in the Indian markets.

How much should I keep in my emergency fund?

Ideally, 6 months of your monthly mandatory expenses. If you are a freelancer or have an unstable income, aim for 12 months. This is the bedrock of financial planning for Indian women.

Why is term insurance necessary if I don’t earn?

If you are a primary caregiver, your “unpaid labor” has immense value. If something happens to you, the cost of replacing those services (childcare, home management) can be a huge financial blow to the family.

How often should I check my investments?

While you should track your progress, don’t check daily. A quarterly review is sufficient to ensure your financial planning for Indian women stays on track with your long-term goals.