Sukanya Samriddhi Yojana 2026: Is It Still the Best Way to Secure Your Daughter’s Future?

As a parent, your vision for your daughter is likely a “Sone ki Chidiya” (golden bird)—a future where her dreams, from Ivy League education to a grand wedding, are never limited by finances. In the landscape of Indian investments, the Sukanya Samriddhi Yojana 2026 remains a titan for conservative wealth building. Currently offering an industry-leading interest rate of 8.2% for Q4 FY 2025-26, it is often the first port of call for any financial advisor.

However, for High-Net-Worth Individuals (HNWIs) and busy professionals, the question isn’t just about the rate—it’s about strategy. In 2026, with evolving market dynamics and the aggressive rise of digital-first assets, is this government-backed scheme enough to beat education inflation? At Nemi Wealth, we believe in looking beyond the surface. Let’s dive into the microscopic details of the Sukanya Samriddhi Yojana 2026, its current benefits, and the “fine print” that often surprises parents.

What is Sukanya Samriddhi Yojana (SSY)?

Launched under the Beti Bachao, Beti Padhao initiative, SSY is a dedicated savings scheme for girls below the age of 10. It is a Sovereign Guaranteed product, meaning your capital is as safe as it gets in the Indian financial landscape.

Key Features at a Glance (2026)

| Feature | Details (As of March 2026) |

| Current Interest Rate | 8.2% per annum (Compounded annually) |

| Minimum Deposit | ₹250 per financial year |

| Maximum Deposit | ₹1.5 Lakh per financial year |

| Tenure | 21 years from account opening |

| Lock-in | Mandatory deposit for 15 years |

| Eligibility | Resident Indian girl child under 10 years |

The Pros: Why Sukanya Samriddhi Yojana 2026 is a Powerhouse

1. The EEE Advantage (The Tax-Free Holy Grail)

In the world of Indian taxation, EEE (Exempt-Exempt-Exempt) status is the gold standard. For the Sukanya Samriddhi Yojana 2026, this means:

- Exempt on Investment: Deposits up to ₹1.5 Lakh are deductible under Section 80C (Old Regime).

- Exempt on Accumulation: The annual interest earned is not added to your taxable income.

- Exempt on Withdrawal: The final maturity amount is 100% tax-free. Unlike Mutual Funds, there is no Long-Term Capital Gains (LTCG) tax here.

2. Industry-Leading Interest Rates

At 8.2%, the SSY consistently outperforms the Public Provident Fund (PPF), which currently stands at 7.1%, and most 5-year Bank Fixed Deposits. For a debt instrument, this is an exceptional “risk-free” return.

3. Disciplined Compounding

Because the money is legally earmarked for your daughter, it prevents “impulse withdrawals” for other family needs. This ensures the corpus remains intact for her 20s, benefiting from two decades of compounding.

The Cons: The Realities You Must Know

While the returns are attractive, the Sukanya Samriddhi Yojana 2026 has specific constraints that might not suit every investor’s lifestyle.

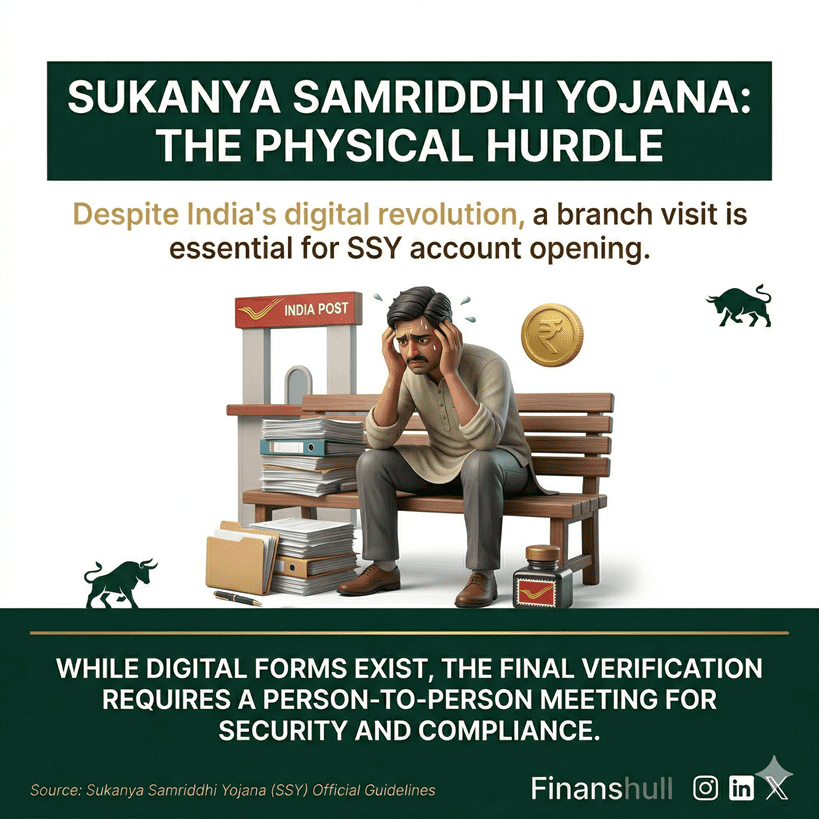

1. The “Physical” Hurdle: Account Opening

Despite India’s digital revolution, you generally cannot open an SSY account 100% online. While banks like SBI, HDFC, and Axis allow you to fill the form online, a physical visit to the branch or a Post Office is almost always required for “wet signatures” and original document verification.

2. Rigid Withdrawal Rules & Liquidity

The most significant drawback is liquidity.

- For Education: You can only withdraw 50% of the balance at the end of the preceding financial year, and only after the girl turns 18 or passes Class 10.

- The Trap: If your daughter needs funds for specialized coaching at age 16 or an expensive sports program, this money is untouchable.

3. No Benefit for the New Tax Regime

If you have moved to the New Tax Regime, the Section 80C deduction is unavailable. While the interest remains tax-free, the initial tax-saving “kick” is gone, making the real rate of return slightly less impactful compared to those in the Old Regime.

💡 Mid-Blog Insight: Want to stay updated on the latest shifts in Indian wealth management? Join our Finanshull community on Instagram for daily reels and expert insights on building a legacy for your family.

Strategic Comparison: SSY vs. PPF vs. Equity Mutual Funds

For a high-intent investor, diversification is key. Relying solely on the Sukanya Samriddhi Yojana 2026 might leave a gap in your goal planning.

| Feature | Sukanya Samriddhi Yojana (SSY) | Public Provident Fund (PPF) | Equity Mutual Funds (SIP) |

| Current Return | 8.2% (Guaranteed) | 7.1% (Guaranteed) | 12-15% (Market Linked) |

| Tax Status | EEE (100% Tax-Free) | EEE (100% Tax-Free) | LTCG Tax (above ₹1.25L) |

| Lock-in | 21 Years | 15 Years | None (Flexible) |

| Liquidity | Very Low | Moderate | Very High |

| Goal Focus | Only Girl Child | General / Retirement | Flexible |

The Nemi Wealth Verdict: Is Sukanya Samriddhi Yojana Enough?

We recommend the Sukanya Samriddhi Yojana 2026 as the “safe base” of your daughter’s portfolio. However, education inflation in India is currently hovering around 10-12%. A fixed return of 8.2%—while excellent for debt—may not fully cover the cost of a specialized degree 15 years from now.

The Professional Strategy:

- Max out the SSY: Put ₹1.5 Lakh annually to capture the 8.2% tax-free yield.

- The Growth Engine: Complement this with a diversified Equity Mutual Fund SIP.

- The Advice Filter: A Wealth Manager doesn’t just “buy funds.” We align your SSY maturity dates with your daughter’s specific education milestones to ensure you never face a liquidity crunch.

Secure Her Future with Clarity

Investing in the Sukanya Samriddhi Yojana 2026 is a noble first step, but a “set and forget” approach is rarely enough for high-achieving families. At Nemi Wealth, we help you bridge the gap between “safe savings” and “inflation-beating wealth.”

Don’t leave your daughter’s dreams to chance. Book a 1-on-1 Personalized Wealth Consultation today to build a roadmap that combines the safety of SSY with the growth of modern markets.

Frequently Asked Questions (FAQs)

1. Can I open an SSY account for my 11-year-old daughter?

No. The account must be opened before the girl child turns 10 years old. There is no grace period.

2. What happens if I miss the minimum annual deposit in 2026?

If you don’t deposit the minimum ₹250, the account is “defaulted.” You can revive it by paying a ₹50 penalty per year of default plus the minimum deposit.

3. Is the 8.2% interest rate fixed for 21 years?

No. The Government of India reviews and announces the interest rate every quarter. While it has been stable, it can fluctuate based on G-Sec yields.

4. Can an NRI open an SSY account?

No. The girl child must be a resident Indian. If she becomes an NRI after the account is opened, it must be closed, or interest will stop accruing.

5. Can I have two SSY accounts for one daughter?

No. Only one account per girl child is permitted. A family can open a maximum of two accounts (one for each daughter), with exceptions for twins/triplets.

Is SSY better than a Child Insurance Plan?

Usually, yes. Child insurance plans often have high commissions and lower transparency. SSY offers higher guaranteed returns with zero management fees.